How much do I need for a downpayment on a house in Seattle? That is the question we get every time we sit down with a new buyer. Saving for a downpayment is one of the biggest roadblocks that homebuyers face when trying to buy a home. This is the same for your first home or your tenth home. And a lot of buyers have a perception that they need 20% down in order to buy a home in Seattle. In this blog, I am going to break down exactly how much money you need for a downpayment for a home here in Seattle.

Downpayment Minimum Amounts for Homes in Seattle

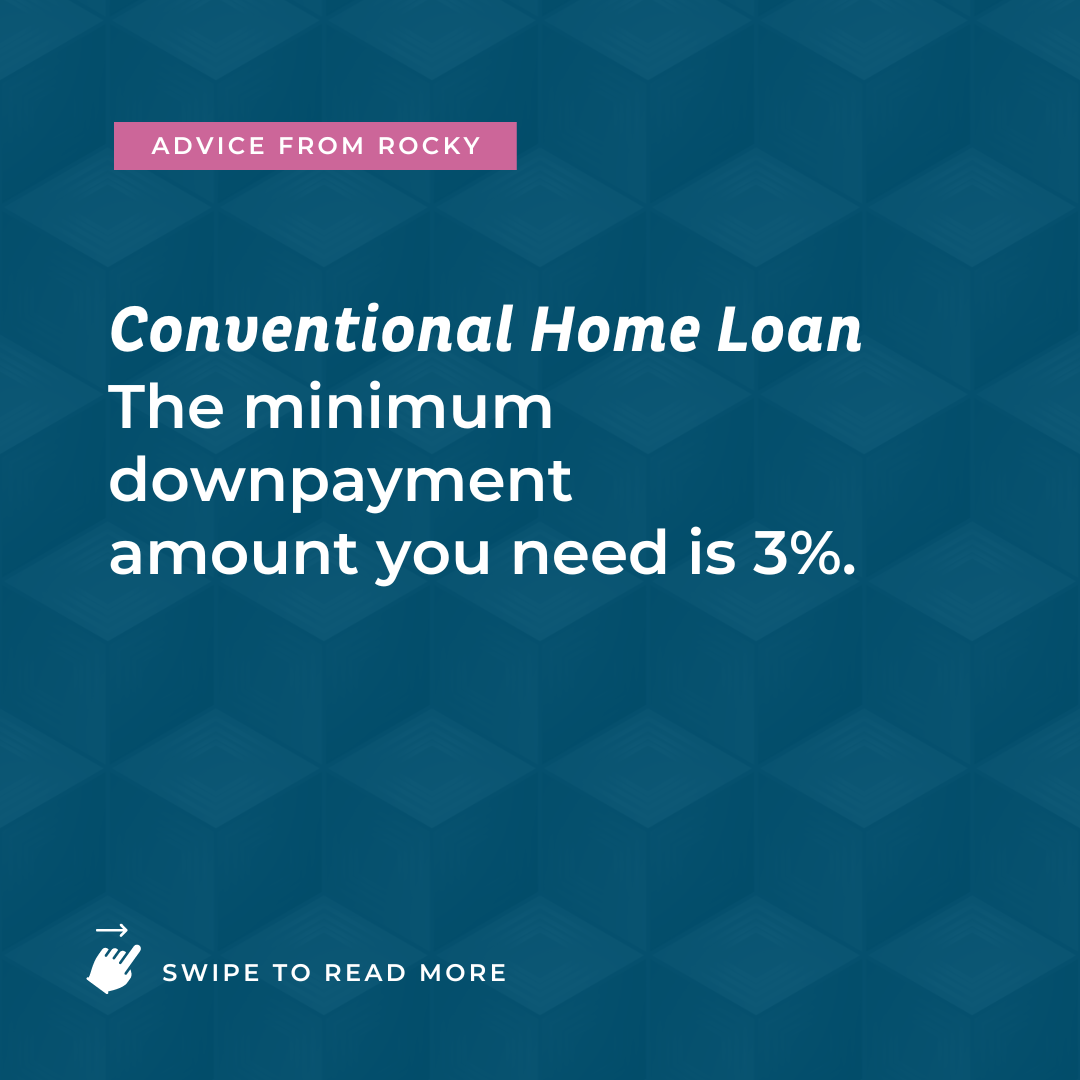

- Conventional Home Loan – 3% of the Purchase Price

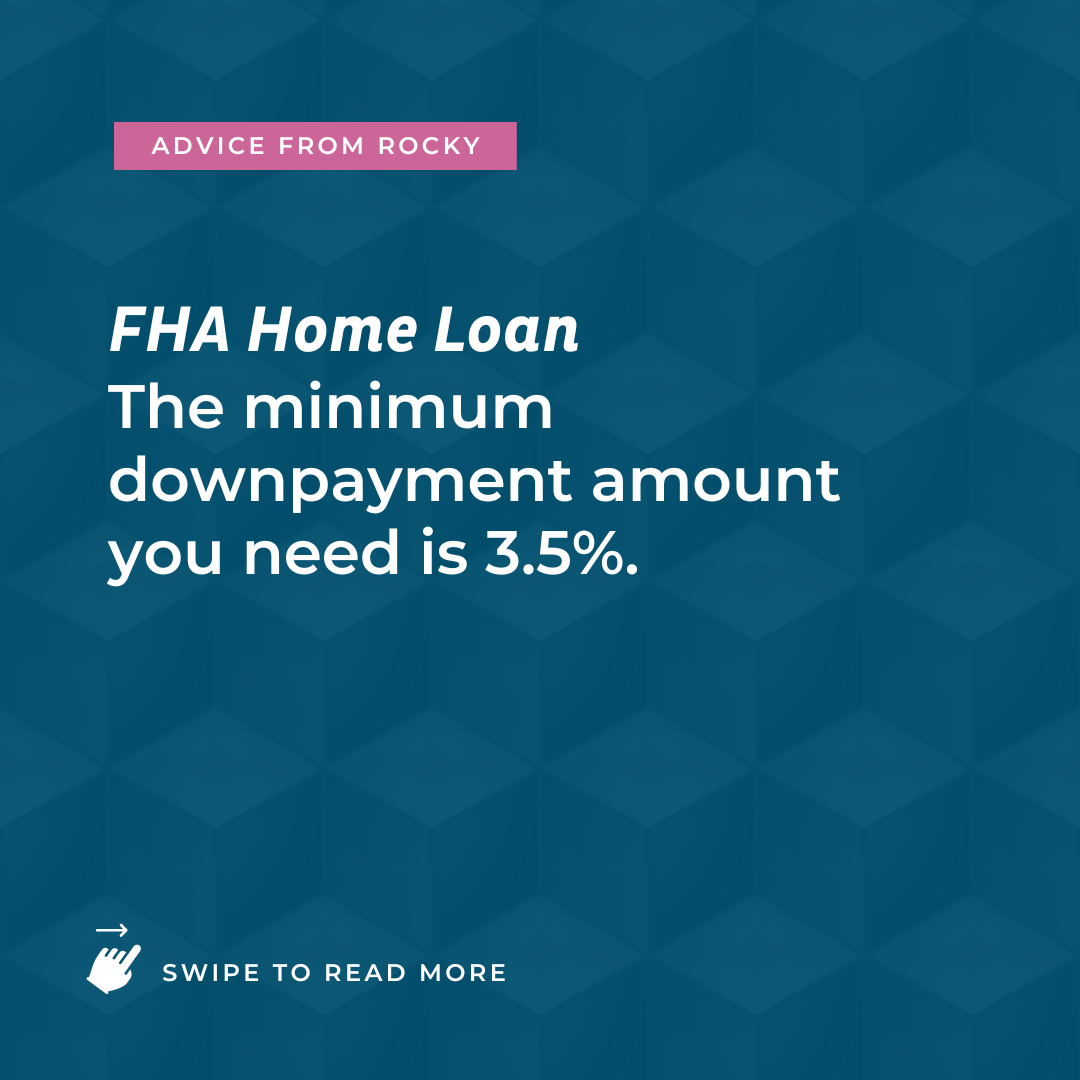

- FHA Home Loan – 3.5% of the Purchase Price

- VA Home Loan – ZERO Down (VA loans are a benefit for military veterans)

- USDA Loans – These types of loans are not really an option in Seattle because we do not have designated rural land in our urban area.

Let’s dive into this and get you the details of what you need for a downpayment for a home.

How Much Do I Need for a Downpayment on a House in the Seattle Area?

Back to the question. How much do I need for a downpayment on a house in Seattle?

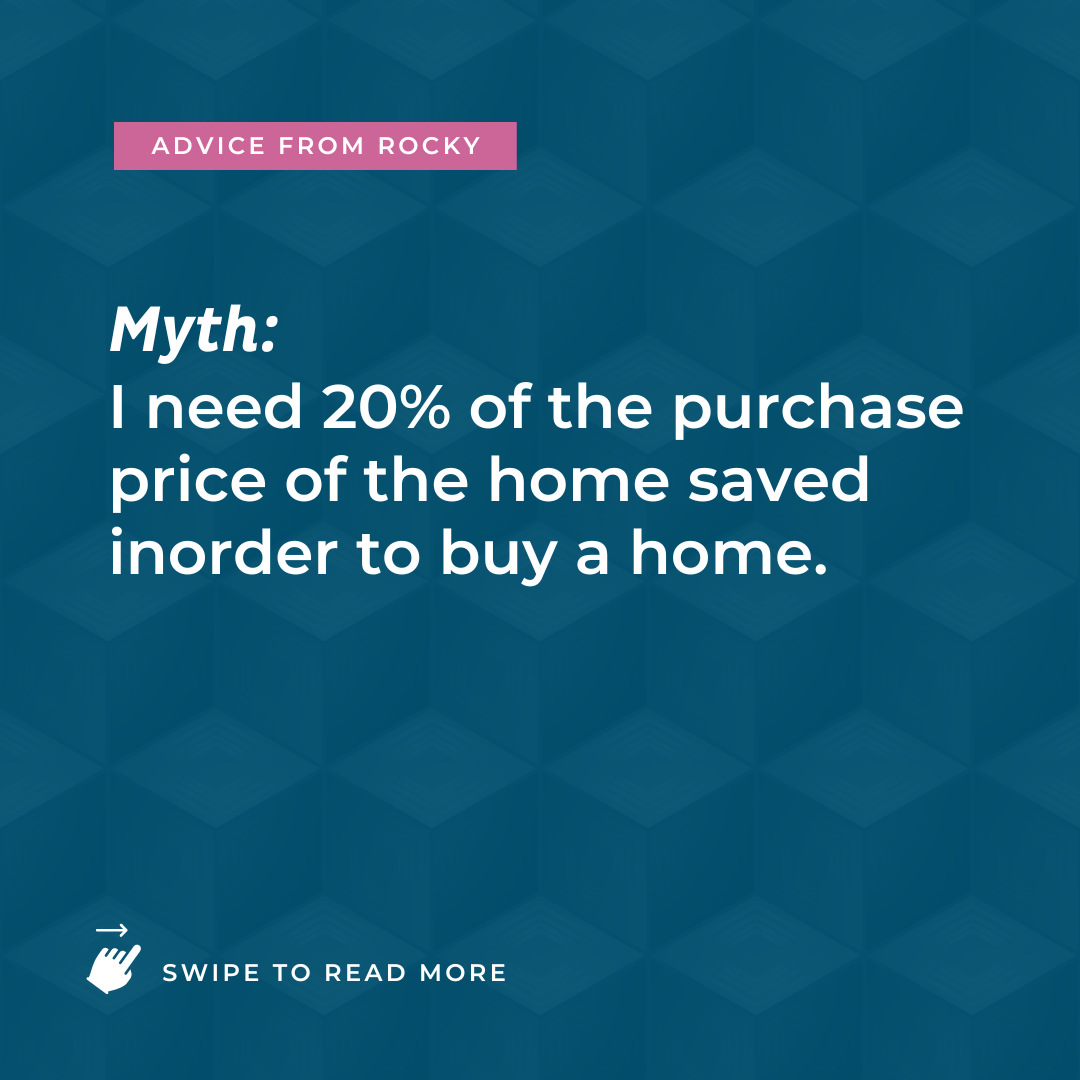

Common Myths – I Need 20% Downpayment of the Purchase Price in Seattle!

And the biggest question we get is “Do I need to save 20% of the purchase price for the down payment?” It is really sad to many of us on the team that Seattle homebuyers think they need large down payments to buy a home in Seattle. While it does make it easier in some cases it is not absolutely necessary. The majority of our first-time homebuyers bought their first home with as little as 5% down. It has only been in the last few years during Seattle’s extreme seller’s market that many buyers needed 20% or even more to win a home in their preferred neighborhood.

The Risk Of Putting Less Than 20% Down for a Home Loan

Buyers have to pay mortgage insurance if they are putting down less than 20% for most conventional and FHA loans. This mortgage insurance can be as high as $350-600 a month on top of your mortgage and interest payment. Technically you should be able to remove that mortgage insurance once you have paid up to 20% of the loan to value. But Lenders are greedy (coughs and looks at the 2008 financial crisis). We are hearing rumors that the only way you can remove the mortgage insurance premium is by fully refinancing your home loan. Big banks suck!

The Benefit of Putting Less than 20% Down For a Home Loan

The first house we bought we bought with an FHA loan and only had 3.5% as a down payment. And of course, we had a mortgage insurance premium. In our first home, we fixed up the interior and planted a huge garden. You know adding a little sweat equity. And a couple of years later we were able to sell that home and buy our big mid-century home in Seward Park. Sometimes it is about getting a foothold on the real estate ladder. And this is how you create generational wealth.

The Shifting Market is Benefiting Homebuyers With Lower Downpayment Options

Right now we are in a shifting market that is benefiting buyers. This is the time for all you buyers out there with a smaller downpayment to make your move. Why? Because there is less competition and you will likely not be competing with anyone when you make an offer on a home.

If you want to find out if now is a good time to buy, my team member Kim just did a video and a blog answering this very question.

How Much Do You Actually Need for a Downpayment on a House in the Seattle Area?

Such a good question. And the answer is “That depends.” What type of loan are you getting? You can put down as low as zero down if you are a veteran and getting a VA loan. Or as low as 3% down if you are buying conventional.

We are going to use Rocky’s new listing in Leschi as a test house to try on different downpayment amounts. Rocky just listed this home for $910,000

Conventional Home Loans – 3% Minimum Downpayment

We just listed this home for $910,000. And believe it or not, you can buy this house with as little as 3% down. You will pay higher interest rates and closing costs. But this is the type of market to get your toe into.

Conventional Downpayment Amounts By Percentages Down

- 5% Down – With a 5% Down payment you can get into this home with just over $45,000.

- 10% Down – If you are putting 10% down you will need about $90,000 for your down payment.

- 20% Down – You would need $180,000 if you were putting 20% down.

FHA Home Loans – 3.5% Minimum Downpayment

For someone buying with FHA, you would need a minimum of 3.5% for your down payment. Once again using Rocky’s new listing as a model you can actually buy a home with a FHA loan product. Many people who are buying with FHA loans have a debt to income or credit issues. For instance, a dear friend of ours was able to buy a home after having to claim bankruptcy from an overwhelming amount of healthcare debt. And the FHA loan limits in Seattle would allow you to qualify for this home. For Rocky’s new listing you can put down as little as $31,000. You can also put more money down for an FHA loan which will help with your monthly payment amounts.

VA Home Loans – ZERO Down Minumum Downpayment

VA loans can be difficult to compete with during a strong seller’s market. The reason is the seller is required to pay for some of the closing costs for a VA loan. Conventional loans don’t have these conditions so they can be more appealing to a seller. But when you are in a market like we have right where there is little or no competition a seller will happily pay those costs. For a VA loan, you can get into a home with zero down. No! Really zero down! You still have some closing costs but this is a great option and an opportunity for many of our Veterans.

Pro-Tip: Consider getting a 7/1 ARM conventional home loan while the Feds keep rates high.

A lot of our buyers are buying homes with what is called a 7 / 1 arm. Meaning their interest rate is lower for the first seven years. Many of the lenders I work with expect interest rates to go back down. And once they do you can refinance into a lower interest rate. And if you want to start chatting with a lender give me a call and I can connect you with some of the best in the city. I will also leave a blog in the show notes about how to get pre-approved for a loan.

Now You Know How Much Money You Need To Get a Home Loan Here in Seattle!

Hopefully, you have learned that you do not need a full 20% downpayment to buy a home in Seattle. Do contact us so we can get you in touch with an amazing lender who lives and works in Seattle. They care bout our clients. Unlike those big banks. The next time you ask yourself “How much do I need for a downpayment to buy a home in Seattle?” just look below for our quick recap of the minimum downpayment amounts.

Downpayment Minimum Amounts for Homes in Seattle

- Conventional Home Loan – 3% of the Purchase Price

- FHA Home Loan – 3.5% of the Purchase Price

- VA Home Loan – ZERO Down (VA loans are a benefit for military veterans)

Want More Information About How to Get Approved For a Loan?

You know we are super passionate about getting our homebuyers educated about the home buying process. Every step of the home buying process has a blog post to go along with it. Including a multitude of blogs about the home loan process.

- Getting Approved For a Mortgage

- What Are Closing Costs

- Competing Against Cash Offers

- Difference Between Pre-Approved Versus Pre-Qualified For a Home Loan

- Getting Your Mortgage Financing In Order to Purchase a Home

Now you can answer “How much do I need to buy a home in Seattle?” You can also always chat with someone on our team and get a personal recommendation for an amazing lender. Give us a call/text at 206-271-0264. Or email us at thediva@teamdivarealestate.com.